Vanilla Option Calculator

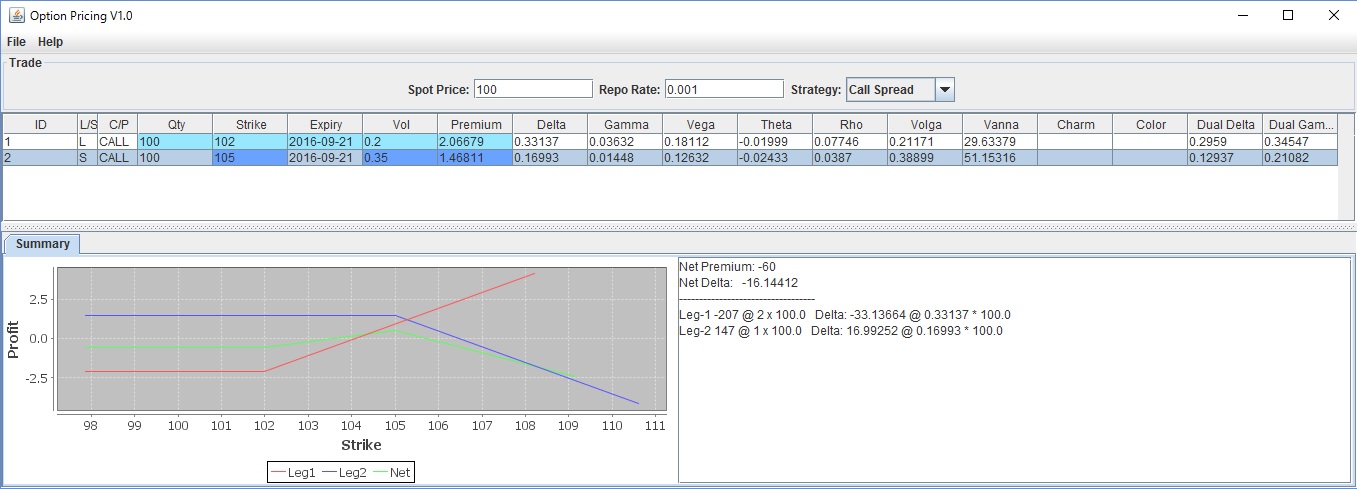

This product demonstrates Java Swing GUI for covering financial industry, especially one of derivatives products, european option. A derivative is a financial instrument that is derived from underlying products which are some other asset, index, event, condition, etc. The reason for supporting the derivative product is one of good products to demonstrate the capability of those technologies. This product calculates european option theoretical price with Black Scholes model. It caluclates not only option premium but also Greeks. The Greeks is to describe how the price of an option changes when something else changes. The details are here. You can access source code here. If you cannot access to the source code, please contact us.